Joe Lowry

Joe Lowry shares with us another insight into the "Opaque Kingdom of Lithium" and is asking the great questions about the underlying fundamentals of supply and demand picture in the Lithium Market in China now. From my personal perspective, I can only share at this point that International Lithium is the part of Vertically Integrated Lithium Business with Ganfeng Lithium and we are talking here that Lithium Technology will power us for the Next Fifty Years and after that Robots. Ganfeng Lithium is taking the security of Lithium Supply as the paramount objective in the next stage of the company's development for the next 10 years. Now reading Joe Lowry and links below you will make your very own opinion why.

International Lithium And Ganfeng Lithium Move Mariana Lithium Brine Project Forward In Argentina.

Mr. Kirill Klip, President, International Lithium Corp. comments, “We have always viewed Argentina as a favorable location for mineral exploration and development and have been able to operate in a mutually beneficial manner with the local people and governments. The results of the recent elections have managed to give foreign corporations greater confidence in the future of business and mineral resource development in Argentina. We welcome the change and look forward to working with the newly elected officials and advancing our Mariana lithium brine project in cooperation with our strategic partner, Ganfeng Lithium. Security of lithium supply is becoming more important as witnessed by recent price increases in China, all in advance of the completion of new battery production facilities announced by Tesla and other manufacturers. We continue to build a vertically integrated lithium business with Ganfeng Lithium to meet the future demand of lithium products that will address the increasing demands for lithium raw materials and chemical products.”

International Lithium Receives Notice of License Renewals for the Avalonia Lithium Project, Ireland

"Mr. Kirill Klip, President, International Lithium Corp. comments, “The Avalonia project joint venture, fully funded by strategic partner Ganfeng Lithium Co. Ltd., (“GFL”), could be of strategic importance to the European Union should a sufficient resource be identified. Clean fuel technologies for motor vehicles are becoming increasingly important to the European Economic Community to tackle climate change and the air pollution crisis in major urban areas. Lithium technology will play a major role when it comes to providing batteries for communication devices, electric vehicles and utility storage systems. Renewable sources of energy such as solar and wind power will also benefit from lithium battery technologies and become more commonplace as the problem of intermittency will be addressed providing steady power from these sources 24/7.” Read more."

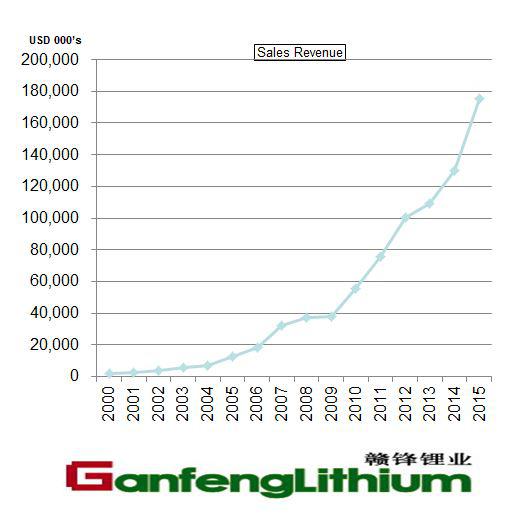

International Lithium Strategic Partner Ganfeng Lithium Has Reached $3.2 Billon Market Cap.

We can write a lot of very passionate words and even cut beautiful music tracks to bring you on the same wave length, but money talks in business in the end. And now we have this very important confirmation of what is going on in "The Opaque Lithium Kingdom." International Lithium strategic partner Ganfeng Lithium has reached $3.2 Billon market cap with the all-time-high price of 58.18 RMB per share. Finally, the real money are going now into the Lithium Sector.

We have two J/V projects financed by Ganfeng Lithium with International Lithium Avalonia in Ireland and Mariana in Argentina. I like what our very talented Team is doing at ILC now. Read More."

Joe Lowry:

The Talison Factor - Part One

The recent run-up in the lithium carbonate prices in China is driven by a supply and demand imbalance that currently exists despite China having more than enough spodumene conversion capacity to meet internal demand and to export when it makes economic sense.

The issue: not enough spodumene from Australia is currently getting to the conversion market. Why - you ask? Great question.

Since being formed in the aftermath of the Sons of Gwalia collapse and insolvency Talison returned spodumene from the Greenbushes lithium operation to the market and as former Talison CEO Peter Oliver said in an interview with Asian Metal in 2012:

“Talison is a leading global producer of lithium and has been supplying a global customer network from the Greenbushes Lithium Operations in Western Australia for over 25 years. In anticipation of sustained growth in lithium consumption, driven primarily by the secondary lithium battery market, Talison has recently doubled its production capacity at the Greenbushes Lithium Operations.”

Talison always maintained in company presentations that they planned to add capacity ahead of demand. Their success supplying the rapidly growing China spodumene converter market drove the bidding war that resulted in Rockwood offering $700 million plus which was an unheard of EBITDA multiple only to be outbid by Sichuan Tianqi who ultimately paid more than $800 million for Talison.

Rockwood later paid $475 million to secure a 49% interest in Talison and the current Talison JV structure became official. Below is a Rockwood announcement from May, 2014:

So why can’t this “spodumene colossus” that has by their own public statements “expanded ahead of demand” adequately supply the China converter market? Certainly it is not a matter of limited capacity. Despite rapid growth in the Chinese market – Talison still has ample capacity to enable converters to meet demand. Through September of this year, Chinese import statistics show a substantial quantity of spodumene is moving to Tianqi yet Tianqi is not supplying sufficient spodumene to converters to meet the carbonate demand of China’s cathode producers.

How do I know? Besides the current carbonate price spike in China, Tianqi’s spodumene customers have told me directly that they cannot get enough raw material to meet the growing demand. In addition, more than one Chinese cathode producer has complained about the shortages and higher prices. Their requests to the “Big 3” for more volume have gone unheard as the brine based majors are “sold out”. The hoped for supplier of last resort (newcomer Orocobre) is still mired in a messy start-up and is not yet capable of producing large volumes or battery quality product.

Global demand for lithium chemicals in 2015 is approximately 160,000 MT of LCE. Lithium ion battery related demand is just under 40% of the market this year and is growing overall in the 15% range as the e-transportation and ESS related markets have finally gained traction. Other (industrial) markets will grow at single digits yielding an overall growth lithium market growth rate in the 10% range. ALB’s often discussed expansion in Chile, by their own admission, will not produce meaningful volumes until 2017. This delay coupled with uncertainty at Orocobre leaves the excess conversion capacity in China as the only viable option to supply growth in the already tight lithium market.

The current situation seems like a perfect opportunity for Talison to increase volume and price at the same time. Unfortunately Talison is now a JV operated by two partners that don’t seem to have a unified strategy. Tianqi is in the enviable position of being the largest converter of spodumene in China and by virtue of their 51% ownership of Talison they profit from the sales of spodumene to their competitors. The hegemony has made Tianqi very unpopular in the China lithium world – the “evil empire” to put the situation in the vernacular of Ronald Reagan.

What possible motivation would Tianqi have for shorting the market once they are certain their own capacity is fully utilized? Do they believe they are better served by shorting the market and driving price up? Is the upside they can make on price more than the profit on the extra volume? In my mind that is doubtful but it only matters what the people making the decisions think. If Tianqi is “managing the market” for their own benefit where does that leave 49% owner ALB?

Talison sales to the two JV owners are supposed to be at an “arm’s length” price yet it is obvious that Tianqi’s interests and ALB’s interest are not aligned when it comes to the Chinese market. ALB should want to see as much volume as possible where Tianqi may believe they benefit more selling less volume and letting the China price rise to beyond the current record levels.

Of course, ALB has already made it clear that they will not expand their hydroxide capacity for a few years and given the limited capacity and less than expected quality performance of their North Carolina hydroxide plant perhaps shorting the conversion market sets them up to negotiate more favorable tolling with contracts with Chinese converters in 2016 – 2019 time frame. I am not a fan of conspiracy theory but you never know.

Certainly the major investment both Tianqi and ALB have made in Talison provide the incentive to fully leverage the asset. On other hand if their behaviors create even the prima facie appearance of “anti-competitive” behavior the partners may want to revisit the current situation.

If you are a spodumene consumer in China you probably long for the good old days when Talison was independent.

Part Two will delve more into the details of the shortage situation but for now I am interested in the comments and ideas from those of you that may have an opinion on the behaviour of Tianqi and ALB in the China market."

No comments:

Post a Comment