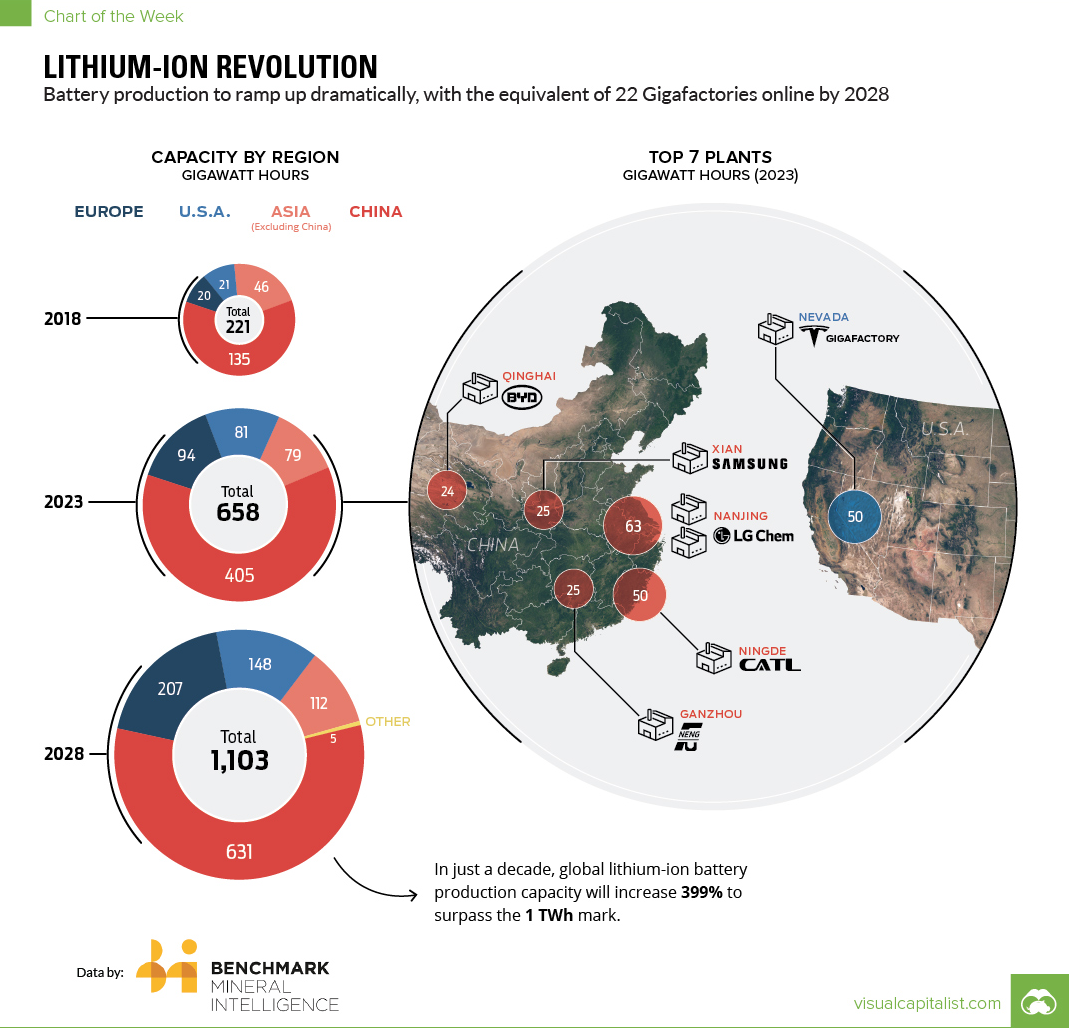

This brilliant infographic was created by Visual Capitalist - Benchmark Mineral Intelligence forecasts that we will see a 400% increase in lithium battery production by 2028. I think that these numbers are very conservative. Let's put it in perspective of electric cars production. 1.1 TWh capacity of lithium batteries annually will allow making 11 million electric cars annually if we assume that 100 kWh will become the industry standard after prices will drop to $100 per KWh.

It will represent only 16% of the worldwide auto sales in 2017, which hit the record of 68.3 million units. So this forecast can hardly be called outrages and, in my personal opinion, even if lithium batteries will be smaller on average than 100 kWh per car, this capacity must be much higher in order to feed Energy rEVolution including electric trucks and buses with much larger batteries and Energy Storage Systems, which will consume even more lithium batteries than transport in the future.

Now let's convert this lithium battery capacity into potential lithium demand. Tesla's 100 kWh lithium battery contains approximately 90 kg of Lithium LCE. Lithium solid state batteries will require even more lithium. 1.1 TWh in lithium batteries capacity can be translated into 990,000 T of Lithium LCE needed annually only for the batteries. Total lithium production in 2017 was 220,000 T LCE. We are getting closer to the forecast by UBS of 1 million T of LCE needed by 2026 annually.

In order to understand better the recent situation in the lithium market, let's try to find out the amount of investment capital which is needed for the increase in lithium LCE annual production from 220,000 T to 1 million T. The price tag can be as high as USD $20 billion. The industry's rule of thumb used to be USD $15k of CAPEX per 1 T of LCE lithium hydroxide annual production, but CAPEX is going up every year, plus we have to account for the projects acquisitions from lithium juniors. Who will finance this lithium expansion? So far, this year 3 out of "Lithium Top Five" are struggling to raise in different IPOs USD $1 billion altogether.

Ganfeng Lithium was going to raise USD $1B in Hong Kong IPO first, then USD $1.5B was discussed last spring, but the actual IPO was only USD $400 million plus this Fall. FMC Lithium division IPO was going to raise USD $1B, but the actual IPO was only USD $300M plus. Now Tianqi is battling with its IPO the market conditions and SQM's legal situation. We have the huge gap between the capital needed for expansion of lithium production and available financing even for the top names in the industry.

"Drama in the Atacama", when 3 out of "Lithium Top Five": Albemarle, SQM and Tianqi - can be affected by the outcome of different legal actions in Chile shows that even relatively well-financed top lithium companies cannot just switch on additional lithium production at will. And we are not even talking about the chemistry soup of lithium brines and technical challenges like with Orocobre production ramping up.

My personal conclusion will be the same as before: any even serious discussion about the coming lithium oversupply is not taking into account the real speed of electrification of transportation and energy industries and that the "Opaque Lithium Kingdom" remains to be a very closely controlled system.

Falling lithium prices are making any competition with the oligopoly of "Lithium Top Five" even more difficult, cash is the real king in our lithium kingdom - and the best projects will be acquired from juniors at the depressed valuations.

Building A Green Energy Metals Royalty Co. TNR Gold: The Battery Boom Has Created A New Lithium Superpower In China.

“They understood so many years back -- in the early 2000s -- that lithium would be driving all of the green energy revolution,” said Kirill Klip, a former executive with Ganfeng’s first overseas partner, International Lithium Corp., who joined the working party in Ireland. “It’s a very hands-on approach, literally -- they were working with our geologists turning over rocks, studying all the lithium boulders,” said Klip, now executive chairman of TNR Gold Corp. Bloomberg.

"At TNR Gold we are moving forward and building A Green Energy Metals Royalty Company by expanding our capital base and business model. Our Royalty with ILC on Mariana Lithium project in Argentina, which is being developed by Ganfeng Lithium, is among core potential royalty streams in our Royalty Portfolio. This is the essence of our business model when industry leaders like Ganfeng and McEwen Mining are the operators on the projects which will potentially generate royalty streams for our Company." Read more.

No comments:

Post a Comment