Joe Lowry provides us with another great insight into the Lithium Market. We have discussed before the growing importance of Lithium Hydroxide, which goes into NCA cathode - chemistry of choice started with Power Tools and now used by Tesla Motors. Joe Lowry adds few new pieces to the Lithium Batteries Supply Chain puzzle for Tesla Motors and other EVs makers today. Follow it closely - this is where bottlenecks are and tension is already pushing up Lithium Hydroxide prices.

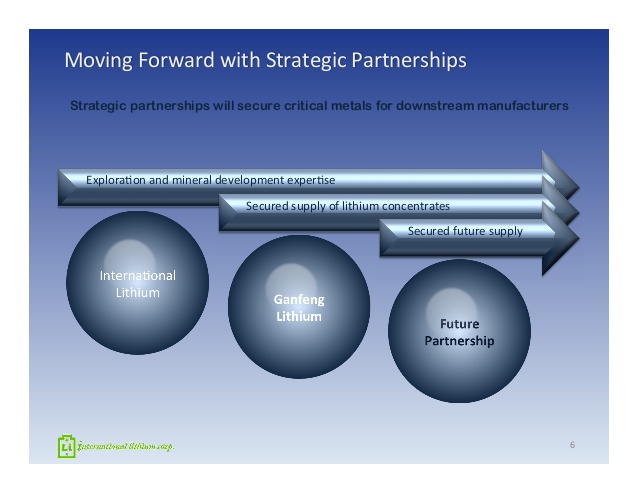

Hedge Funds and Venture capital are going on the fishing trips Upstream now searching for the producers of components and materials which are going to supply the exponential growth of this rEVolution ignited by Elon Musk. China is happen to be the fastest growing strategic commodity supplier again here. 75% of battery Grade Lithium Hydroxide production is controlled by China now. International Lithium strategic partner Ganfeng Lithium has built state-of-the-art Lithium Hydroxide production facilities with 6,000 T/Y output in China. International Lithium is building the secure supply for Ganfeng Lithium and our two J/V projects in Ireland and in Argentina are financed by this Chinese giant.

International Lithium Corp. - A Green-Energy Metals Company.

"I have written extensively about International Lithium and our strategic partner Ganfeng Lithium. Our J/Vs in Argentina and Ireland are financed by this giant from China and we have very important access to the technology. Basically we are building the secure supply chain for Ganfeng Lithium using their expertise in raw materials needed for production of battery grade lithium from the very beginning. Our brine bulk sample from Mariana is being tested at Ganfeng state-of-the-art R&D facilities in China and in Ireland we have identified 22 exploration targets. Now, according to our latest NR, we are waiting for the approval of the budgets for both projects to be rapidly advanced after very encouraging results were received from the last exploration stage this year.

Today I would like to show you another side of International Lithium. We have the very strong technical team headed by our CEO Gary Schellenberg. Anthony Kovac - our COO and John Harrop - our VP of Exploration are among very few top level exploration managers and geologists in lithium sector. This Team depth has allowed International lithium to attract Ganfeng and strike two major J/V deals in all our industry. These days we are getting the first fruits of this very hard work. Coming volume shows that market is waking up and we are receiving at least some recognition of the value we have been building all these years.

I am talking a lot about the security of lithium supply and Tesla Lithium Hydroxide Supply Deal is another proof and was noticed by market overnight. Now venture capital is knocking on all doors chasing the upstream supply chain for electric cars and Energy rEVolution.

We have another great project at International Lithium: Mavis Lake Lithium And Tantalum Project which is located in mining friendly Canada in the area with excellent infrastructure and very encouraging initial exploration results with high grade Lithium and Tantalum. It will be our next strategic advance for the company. With J/Vs moving forward we are looking for the strong Strategic Partner to develop this project for the potential supply of this strategic commodity for the ongoing Next Industrial rEVolution. West will wake up one day to the fact that China has managed to control now not only over 90% of REE production, but 75% of Battery Grade Lithium Hydroxide as well.

Security of Supply means exactly this - Security. When the price is taking the second consideration and availability of critical materials is taking the central stage. My personal mission is to make this Security happen for the Western world for real as well, even if this part of the World still lives by HFT rules and Q by Q performance reflecting the coming bonuses. Our Asian friends are beating us all here with the state-level plans looking for The Next Fifty Years and building new strategic industries like Electric Cars in China.

We have Elon Musk, we need more like him, but it is a very good start. Our strategic partner for Mavis Lake is waiting somewhere in between of latest Q performance reviews. If you know the one - you know whom to call. Now I do not have really to explain any more What Is Lithium For - Elon Musk has made the great job and every single Tesla Model S is the best moving ad of the things to come. All cars will be electric and it will be very soon. And by the way any new hard rock mine for Lithium will take 5-7 years to build Lithium brine operations will take 4-5 years at best.

Why International Lithium? You can check presentation above. Read more."

Joe Lowry:

China Lithium Supply to Tesla Growing Rapidly

"Japan is by far the largest market for lithium hydroxide used in lithium ion batteries. The graph below shows the growth in imports of lithium hydroxide from 2013 to July, 2015. Over 85% of the hydroxide imported to Japan is used for lithium ion battery related production such as the NCA cathode produced by Sumitomo Metal Mining and others in Japan that ultimately goes into Panasonic battery cells bound for Tesla. The other major use for lithium hydroxide is multi-purpose grease production.

Just three years ago FMC had ~90% share of the lithium hydroxide going into the Japanese ion battery market and could price at a premium. Rockwood's entry into the battery quality segment brought lower prices beginning in 2013 and a decreased share for FMC.

Just three years ago FMC had ~90% share of the lithium hydroxide going into the Japanese ion battery market and could price at a premium. Rockwood's entry into the battery quality segment brought lower prices beginning in 2013 and a decreased share for FMC.

In early 2014 Tesla and Panasonic realized that FMC and Rockwood were not expanding to meet their long term demand forecast. Key participants in Tesla's lithium supply chain turned their attention to China. In a relatively short period multiple suppliers in China were qualified and began shipping to Japan. FMC's share has continued to decline. It is now approximately one third of the battery market.

Imports to Japan from both the US and China are growing but China imports are growing at a much faster rate. Despite cost and VAT disadvantages the Chinese suppliers are willing to price lower than their US competitors to gain share.

If this were a normal commodity market, you would expect the lower cost brine producers to leverage their cost advantage; however it has become obvious that FMC and Rockwood are not willing to invest if Tesla is not going to make firm long term purchase commitments. Tesla's supply chain now has to deal with a larger number of suppliers. Instead of increased demand lowering their lithium acquisition cost - just the opposite is happening.

The Tesla Gigafactory will only exacerbate the need to buy higher volumes from the producers with larger capacity but higher costs.

The supply deal recently announced where Tesla will allegedly source lithium hydroxide from clay based production at a yet to be determined point in the future is another odd twist to the Tesla lithium story.

The Gigafactory's massive scale will likely help Tesla produce lower cost batteries than they currently source from Panasonic but their "unique" lithium supply strategy only ensures that they will pay more for lithium. There is a real possibility they may face spot shortages in 2018 and 2019 that limit their battery production. Call it the curse of a very long supply chain.

Another point to consider is that China now uses more lithium for cathode production than Japan and Korea combined. Just a few years ago, China was a distant #3. Things change rapidly in China. Fortunately for Tesla, the Chinese cathode market currently focuses on products and formulations that require lithium carbonate but as that market evolves the situation is likely to change. Lithium hydroxide use for cathode in China is still in the beginning stages.

Tesla is playing a dangerous and foolish game with one of their most critical raw materials."

No comments:

Post a Comment