Bloomberg

Guest post:

Energy rEVolution Electric Race Supercharging Commodities Super Cycle.

Imitation is superior to creation. The truth is that the former is simply more efficient than the latter. That truth grants imitators overwhelmingly better returns on time, effort and money than creation grants to the innovator.

Spotify was not the first digital music service, nor did Apple possess the first portable music player. Diners Card created credit cards but lost the market to MasterCard/Visa and while EMI created CAT scans today the market is dominated by General Electric. Facebook and Google; further examples of companies allowing their seniors to establish a market before committing and eventually overtaking the market space via superior application of lessons learned at the cost of the innovator.

Consider the following: In 1984, Chrysler invented the modern minivan. Less than a decade later, GM introduces its Spark minicar, while a Chinese imitation ‘QQ’ comes out within the same year and outsells the original six to one in mainland China.

The year Tesla released its first Model S? 2012.

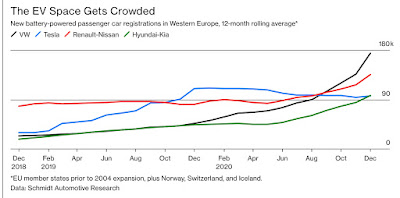

Tesla, the undeniable first-mover of a sensible scale within the EV space, may hold the consolidated advantage in the market with its fostered cult-like scale of pop-appeal and formidable deployment, but a late-mover advantage and its natural goldmine of hindsight is an envious high ground to behold. Tesla will therefore very well see its competitors slingshotting their way over the finish line for the largest market share for EVs in the coming years.

Case in point: at half the price of a Tesla Model 3, the Renault Zoe is already hailed for having overtaken the Tesla Model 3 to win the title of Western Europe’s biggest-selling BEV in 2020.

Tesla’s competitors regaining the title of potatoes and mash to the wider consumer is great for three parties: the consumer, the competitor and the commodity supercycle bull.

The European Union has led the global drive to combat global warming by pledging to become carbon neutral by 2050. This will involve transitioning the bloc to a utilities-based energy model in which consumers will use clean renewable energy. It stands to reason that the EU in turn will serve as a pioneer continent for the world’s wider transition towards electrified transportation methods. The success of Tesla's competitors within this continent, therefore, very well bodes ill for Tesla’s global future.

As we’ve written previously, with smart plays like modularising battery supply and leveraging its economies of scale, Volkswagen, in particular, holds the greatest chance of slingshotting its progress on the back of imitation before leveraging its greater resources to bear the costs of developing new technologies when the time requires it to forge ahead of the back. Indeed, Deutsche Bank projects VW could beat Tesla’s global EV sales by next year.

Holger Zschaepitz @Schuldensuehner

Rising pressure on Tesla signals lower prices in the EV space, particularly with battery prices dropping faster than projected (97% from 1991). Lower prices in turn mean EVs become more affordable; a particular sticking point for the EV space - and Tesla’s particular Achilles heel - which still remains dominated by expensive prices for the wonder consumer. Parabolic numbers of EVs sold, not to mention relevant charging infrastructure, drives greater pressure on the raw materials and minerals required not just in terms of quantity of material but the number of customers and intensity of competitive bidding on it.

So we see, that during the past three months, major banks and hedge funds have bet on a commodities bull market as government stimulus kicks in and the pandemic recedes.

‘Prices of copper, nickel, cobalt, platinum and rare earth elements are all inflating as electric vehicles and the wider electrification trend starts pulling on constrained resources. Nickel prices just closed shy of a five-year high, copper is up 30% from pre-COVID levels, and cobalt has jumped 25% in value in 2021 alone.’

Copper, in particular, is a major component of motors, batteries, inverters, wiring and recharging. Some electric vehicles can contain over a mile of copper wiring in internal windings.

Peter Tertzakian, in his article for the Financial Post, goes on to make an excellent point: ‘I should note that the solar industry’s achievements are often quoted as a template to how fast clean energy costs can come down. But let’s be careful. Made from silicon, the most plentiful element in the earth’s crust (think sand), solar panels don’t have a resource constraint problem. Many of the vital metals and minerals needed to electrify transport and other industrial segments of our economy don’t enjoy the same abundance.’

Our Company, TNR Gold is plugged into this Energy rEVolution with our Royalty Holdings on giant Copper and Lithium projects under the management by industry leaders like Ganfeng Lithium and McEwen Mining.

Kirill Klip stated in his recent letter to TNR Gold shareholders: “Our forward-thinking approach is allowing us to integrate our strategic portfolio with the international capital markets, while maintaining efforts to minimize dilution for all our shareholders. During these favourable macro-economic conditions for gold and green energy metals, we have been enjoying an entirely new level of attention and participation from certain financial institutions. This will allow us to accelerate the development of the Shotgun Gold Project as well as continue to advance our royalty portfolio within the next chapter of business: Green Energy Metals. We maintain the potential of adding to our core royalty holdings on the Los Azules Copper Project with McEwen Mining and the Mariana Lithium Project under the management of Ganfeng Lithium.”

TNR Gold holds NSR royalties on projects containing copper, gold, silver and lithium metals. TNR Gold does not have to contribute any capital for the development of the Los Azules Copper Project and the Mariana Lithium Project. Neither does our NSR Royalty depend on the size of International Lithium’s potentially diluted ownership in the Mariana Lithium Project. The essence of our business model is to have industry leaders like McEwen Mining and Ganfeng Lithium as operators on the projects that will potentially generate royalty cashflows to contribute significant value for our shareholders.”

TNR Gold Investor Presentation - Building The Green Energy Metals Royalty and Gold Company from Kirill Klip

Please read my legal disclaimer. There is NO investment advice on any Kirill Klip feeds and blog. Always consult a qualified financial adviser before any investment decisions.

Do Your Own Research.

No comments:

Post a Comment